illustration from Napkin Finance

illustration from Napkin Finance

In today's dynamic economic landscape, taking control of your personal finances is not just an option—it's a necessity. Mastering your money is the key to unlocking financial security, reducing stress, and ultimately building the life you envision. This isn't merely about spreadsheets and numbers; it's about making deliberate choices aligned with your values and long-term aspirations. Whether you're navigating early career finances, saving for significant milestones, or planning for a comfortable retirement, a solid understanding of personal finance principles is your essential foundation. This comprehensive guide will empower you with actionable strategies across the core areas of personal finance, putting you firmly in the driver's seat of your financial future.

Laying the Foundation: The Core Pillars of Personal Finance

Think of your personal finance journey as building a sturdy house. Each component is crucial and interconnected, contributing to your overall financial stability and growth:

- Budgeting & Mindful Spending: Understanding where every dollar goes.

- Saving & Emergency Preparedness: Creating a safety net and funding goals.

- Debt Management: Strategically eliminating liabilities.

- Credit Health: Building and maintaining a strong financial reputation.

- Investing for Growth: Putting your money to work for the future.

- Retirement Planning: Securing long-term financial independence.

- Setting Financial Goals: Defining your targets and creating a roadmap.

Developing proficiency in these areas requires dedication, continuous learning, and consistent action. Let's explore each pillar in detail.

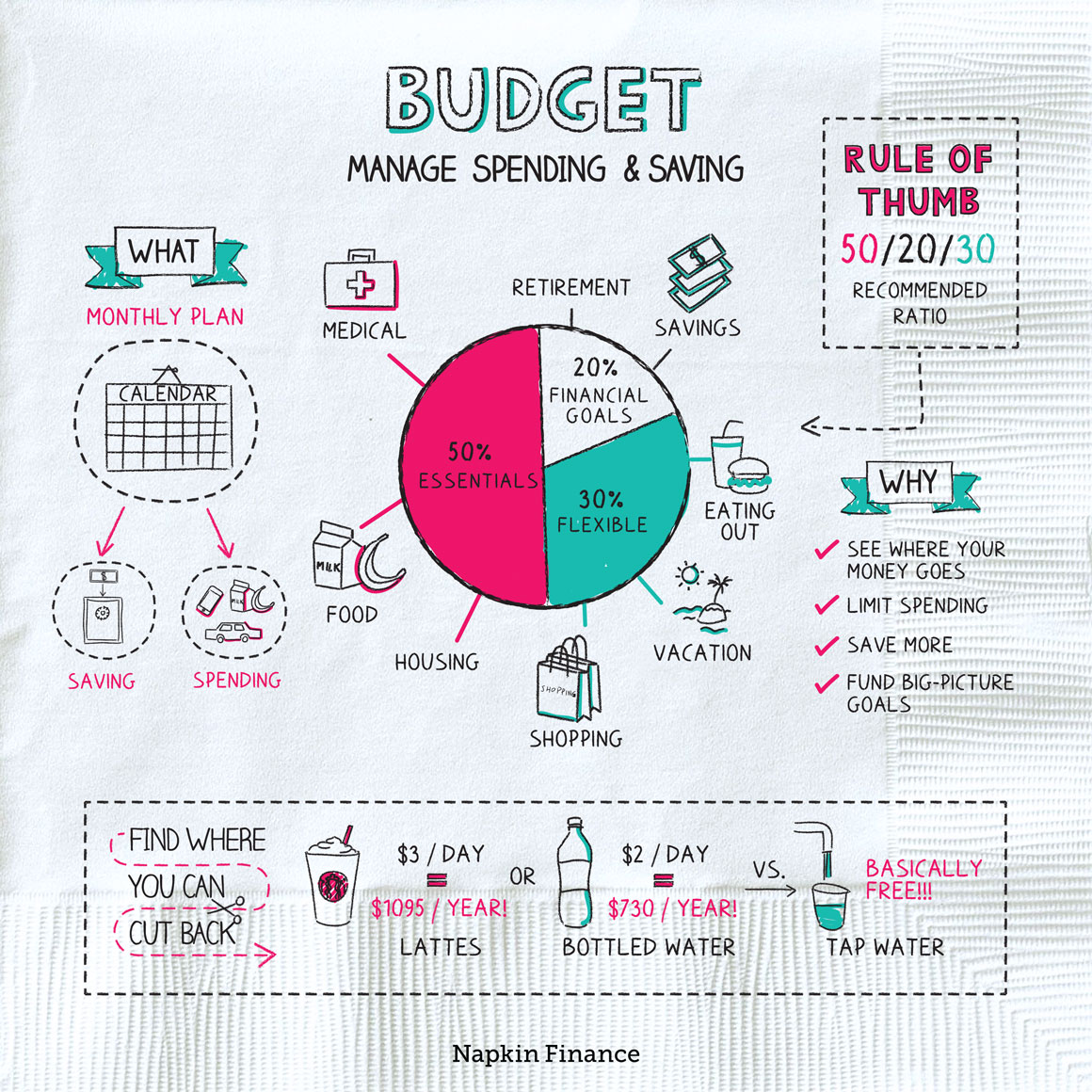

Pillar 1: Mastering Your Cash Flow Through Budgeting

The absolute starting point for taking control is creating and following a budget. A budget is your financial GPS, guiding your income towards your priorities instead of letting it drift aimlessly. It provides clarity, enables conscious decision-making, and is fundamental to achieving any financial goal.

Why Budgeting Isn't Optional

- Full Visibility: Reveals exactly where your money is being spent – often uncovering surprising patterns.

- Empowered Choices: Allows you to intentionally direct funds towards savings, debt reduction, or investments.

- Goal Acceleration: Makes saving for down payments, vacations, or investments a tangible reality.

- Peace of Mind: Reduces financial anxiety by giving you a clear picture and plan.

Finding Your Ideal Budgeting Method

The best budget is one you'll actually stick to. Explore different approaches:

- The 50/30/20 Rule: Simple allocation: 50% Needs, 30% Wants, 20% Savings/Debt Payoff. Easy to implement.

- Zero-Based Budgeting: Every dollar has a job. Income minus expenses and savings must equal zero. Offers maximum control but requires meticulous tracking.

- The Envelope System: A tactile method using cash envelopes for variable spending categories. Excellent for curbing overspending.

- Digital Tools: Utilize apps (Mint, YNAB, Personal Capital) or spreadsheets for automation, tracking, and insights.

Effective Spending Tracking

Budgeting is theoretical without tracking. Log your expenses diligently for at least a month using your chosen method. This crucial step highlights spending habits and identifies potential areas for optimization.

Pillar 2: Building Your Financial Cushion & Funding Goals

Saving is more than just accumulating cash; it's about building resilience and opening doors to future opportunities. The most vital savings goal is establishing a robust emergency fund.

The Non-Negotiable Emergency Fund

Life is unpredictable. Unexpected events—job loss, medical bills, major home or car repairs—can strike at any time. An emergency fund is your shield, preventing you from derailing your progress by resorting to high-interest debt during a crisis.

How Much Protection Do You Need?

Aim for 3-6 months' worth of essential living expenses. Assess your job stability, dependents, and income variability to determine the right target. Calculate your monthly essentials (housing, utilities, basic food, insurance, debt minimums) and multiply.

Where to Keep Your Safety Net

Accessibility is key, but temptation should be minimized. A high-yield savings account is ideal. It offers liquidity, FDIC insurance for safety, and earns modest interest, unlike volatile investments.

Setting Your Sights on Other Savings

Once the emergency fund is solid, define and save for other goals:

- Down payments (home, car)

- Future education costs

- Dream vacations

- Major purchases or renovations

Break these down into achievable monthly targets and automate transfers to make saving consistent and effortless.

Pillar 3: Conquering Debt and Reclaiming Cash Flow

High-interest debt is a major impediment to wealth building. It siphons off money that could be used for saving or investing. Strategically managing and eliminating debt is paramount to freeing up your financial resources.

Distinguishing Debt Types

- Wealth-Building Debt (Potentially 'Good'): Used to acquire assets that may appreciate or generate income (e.g., a mortgage, certain student loans, well-managed business loans).

- Consumptive Debt ('Bad'): Used to finance depreciating goods or everyday spending (e.g., credit card balances, payday loans, car loans beyond your means). Prioritize eliminating this type.

Effective Debt Payoff Strategies

Choose the method that best motivates you:

- Debt Snowball: Pay off debts smallest balance first, regardless of interest rate. Provides psychological wins to maintain momentum.

- Debt Avalanche: Pay off debts highest interest rate first. Saves the most money on interest over time.

Consistency and applying extra payments are critical to both methods.

Smart Debt Management Tactics

- Consolidate/Refinance: Explore consolidating high-interest debts into a lower-APR loan or using balance transfer offers (understand the terms). Refinance mortgages or student loans if rates are favorable.

- Communicate with Creditors: If facing hardship, contact lenders; they may offer hardship programs or payment plans.

- Halt New Debt: Avoid taking on more debt while actively paying down existing balances.

Pillar 4: Building and Protecting Your Credit Health

Your credit score is a vital representation of your financial reliability. It impacts borrowing costs, insurance rates, and even rental applications. A healthy score is a powerful asset.

The Importance of Your Credit Score

Lenders use scores (like FICO or VantageScore) derived from your credit reports to assess risk. A higher score signals lower risk, granting you access to better terms on loans and credit products when needed.

Key Factors Influencing Your Score

- Payment History (35%): Paying bills on time is paramount.

- Credit Utilization (30%): Keep balances low relative to your credit limits (ideally under 30%).

- Length of Credit History (15%): Older accounts in good standing help.

- Credit Mix (10%): A blend of credit types can be positive, but is less impactful than payment history/utilization.

- New Credit (10%): Opening multiple accounts rapidly can temporarily lower your score.

Strategies for Credit Improvement

- Pay Everything On Time: Set reminders or automate payments.

- Reduce Credit Card Balances: Pay more than the minimum and keep utilization low.

- Monitor Your Reports: Get free annual reports from AnnualCreditReport.com and dispute inaccuracies.

- Keep Old Accounts Open: Don't close accounts with no annual fee if they add to your history and available credit.

- Apply for Credit Judiciously: Only when necessary.

Pillar 5: Growing Wealth Through Strategic Investing

While saving provides stability, investing is where your money can truly grow over the long term and outpace inflation. It's essential for funding future goals beyond your emergency fund.

Why Investing Matters for Long-Term Growth

- Combating Inflation: Protects your purchasing power over time.

- Harnessing Compounding: Earn returns on your initial investment AND the accumulated returns, leading to exponential growth.

- Funding Major Goals: Essential for retirement, education, and achieving financial independence.

Understanding Key Investment Avenues

Navigate the options by understanding the basics:

- Stocks (Equities): Ownership in companies. Higher potential return, higher risk.

- Bonds (Fixed Income): Lending money to entities. Generally lower return, lower risk than stocks.

- Mutual Funds & ETFs: Pooled investments offering diversification across many assets. Index funds (tracking market indexes like the S&P 500) offer broad diversification and low costs.

- Real Estate: Physical property. Can generate income and appreciate, but requires significant capital and management.

Risk Tolerance and Diversification: Your Investment Compass

Assess your comfort level with potential losses (risk tolerance). This, along with your time horizon, dictates your asset allocation (mix of stocks, bonds, etc.). Diversification—spreading investments across different asset classes, industries, and geographies—is crucial for mitigating risk.

Starting Your Investment Journey

- Open a Brokerage Account: Use online platforms (Vanguard, Fidelity, Schwab, etc.) to access investment products.

- Consider Robo-Advisors: Automated services that build and manage a diversified portfolio based on your profile (e.g., Betterment, Wealthfront). Great for beginners.

- Start Small, Invest Consistently: You don't need a fortune. Set up automatic contributions to leverage dollar-cost averaging.

- Focus on the Long Game: Resist reacting to short-term market volatility. Time in the market is generally more important than timing the market.

Pillar 6: Designing Your Secure Retirement

Retirement may seem distant, but starting early is the single most impactful factor in securing your financial future. The magic of compounding works best with time.

The Power of Starting Early

Even modest contributions made early can grow significantly over decades thanks to compounding. Delaying means needing to save disproportionately larger amounts later on.

Leveraging Tax-Advantaged Retirement Accounts

Maximize contributions to these powerful savings vehicles:

- 401(k) (Employer-Sponsored): Pre-tax contributions lower current taxable income. Always contribute enough to get the full employer match—it's free money!

- Traditional IRA: Contributions may be tax-deductible; earnings grow tax-deferred. Withdrawals in retirement are taxed as ordinary income.

- Roth IRA: Contributions are after-tax, but qualified withdrawals in retirement are tax-free. Excellent if you anticipate being in a higher tax bracket later.

Understand the contribution limits and withdrawal rules for each.

Estimating Your Retirement Needs

How much will you need? While rules of thumb exist (e.g., 80% of pre-retirement income), use retirement calculators to get a more personalized estimate. Factor in inflation and potentially significant healthcare costs.

Beyond Retirement: Holistic Future Planning

Comprehensive planning includes:

- Estate Planning: Basic wills, powers of attorney, and potentially trusts (important as assets grow).

- Adequate Insurance: Protecting your income and assets with health, disability, life, home/renters, and auto insurance.

Bringing It All Together: Your Financial Roadmap & Ongoing Review

Mastering personal finance is a continuous journey of learning and adaptation. Begin by defining clear, measurable goals. Establish your budget, build your emergency fund, and systematically eliminate high-interest debt. Then, commit to consistent long-term investing aligned with your risk tolerance and time horizon, leveraging tax-advantaged retirement accounts. Remember to regularly review and adjust your plan—at least annually—as life circumstances, goals, and market conditions change.

Take Action: Build Your Financial Future Today

Don't be intimidated by the scope of personal finance. Start small. Choose one area—like creating a simple budget or automating a savings transfer—and take action today. Every single step forward, no matter how small, builds momentum towards lasting financial well-being and security. Educate yourself, stay disciplined, and build the financially free future you deserve.

Ready to begin? Challenge yourself this week to track every single expense and identify one specific area where you can reduce spending. Share your biggest personal finance challenge in the comments below!

Published on June 17, 2025

reference: General Financial Principles & Best Practices

Share to:

![]()

![]()

![]()

![]()

![]()

Gema

Wordsmith and content writer passionate about creating high-quality content that informs, entertains, and inspires. Let me bring your brand's story to life.

All stories by : GemaRelated Posts

-

February 9, 2025

Mastering Your Finances: A Comprehensive Guide to...

-

July 6, 2025

Decoding the Market: Dan Nathan & Carter Worth on...

-

March 7, 2025

Decoding the Debt Dilemma: A Gen Z & Millennial Gu...

0 Comments